Last week in discussing overhead allocation in conjunction with quoting new business, I promised an article on zero-base budgeting. Not to keep people waiting, here goes.

What is zero-base budgeting? In layman’s terms, it involves budgeting by rebuilding an organization on a piece-by-piece basis. It starts by proverbially dragging everything out into the parking lot and reconfiguring the firm from scratch. This is all done “on paper”, you start with a clean slate and add back segments incrementally. The goal of the exercise is to identify the incremental profitability of various segments of an organization.

When is it used? In my experience, it is typically used in distressed situations where an organization needs to figure out an optimal configuration in order to continue as an ongoing entity. Some organizations use the approach on a regular basis as their method of budgeting, but the focus here is using it on an “as-needed” basis.

Is this a painful exercise? It depends on your definition of painful, but most likely, the answer is yes. This process involves at least one full day for an entire management team spent scrutinizing an organization at every function. However, it is extremely insightful since it is a good way of identifying where the resources are utilized instead of analyzing resources in the aggregate.

What is needed beforehand? A lot! There is significant preparation that needs to be conducted prior to gathering the top managers. This critical prep work requires the finance / accounting teams (perhaps assisted by an outside expert) to produce all the information that will be used when all the key people are assembled. The goal is to have unbiased information so people don’t get side-tracked and can stay focused on the key points.

Rules of Engagement – Before starting, it is important to remember the key rules, which are as follows:

- Start from scratch. No backing into numbers

- No Sacred Cows

- Positions Only. Proper Names can only be used to describe a position (ex like “Mark”)

- No significant operational improvements assumed.

- Go with the flow. The process is iterative, and it can be difficult.

Example – Manufacturing

We will look at our hypothetical manufacturer, ACME Corporation, to guide us through the high level process.

Prep work needed: Here are some of the facts and figures that might be needed in order to properly and efficiently conduct the exercise. The exact needs would be dictated by the specific nature and makeup of the organization.

- Variable Income and Expenses by Product. This one is absolutely critical, the key is to strip out any fixed costs, so only truly variable costs are used, whether it is material, labor, electricity, and supplies.

- Sales by customer by product. If customers have different pricing programs for various products, this information would be needed as well.

- Understanding of drivers for each expense (i.e. travel required per salesperson; insurance costs for property, liability, workers comp; software licenses per user; benefit costs per employee, etc.).

- Listing of all personnel and compensation by department.

- Listing of all assets, their value, depreciation and any associated payments (leases, term loans).

The process: The starting point is dependent on the nature of the business. You could look at a business by each major customer / division, it could be by product types. If you have a company with multiple types of products, you might pick a flagship product as the first level.

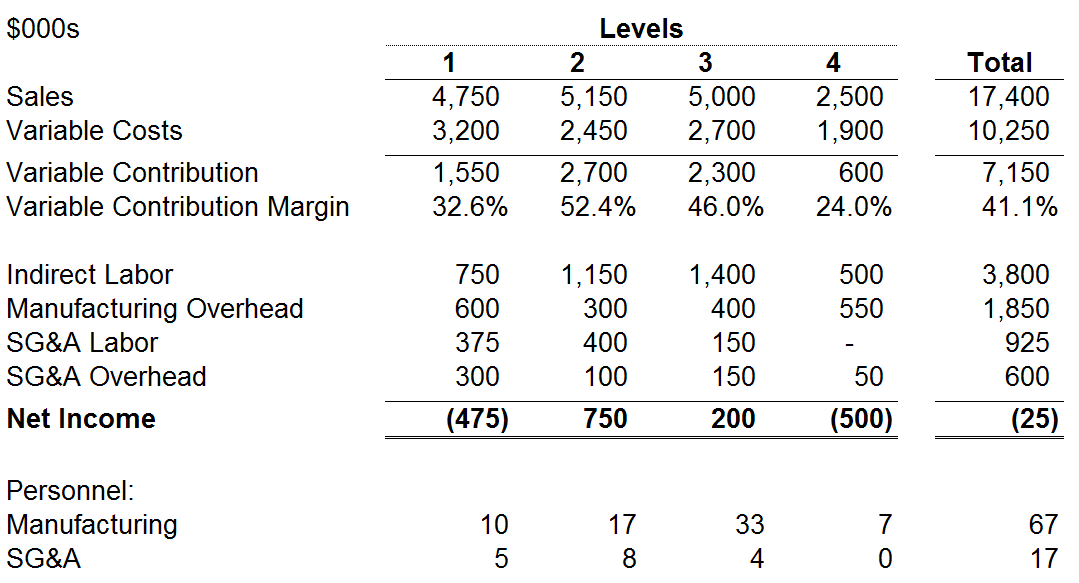

Level 1 – For instance, ACME makes cell phone cases and cassette tape cases, among other products and sells to a very broad assortment of customers. The flagship product is cell phone cases, so this is selected as the first category. Now, the sales and variable costs for these products have to put into the first column.

Next, all the other fixed costs and resources need to be contemplated, these include:

- Personnel – A president, who might also act as sales manager and a plant supervisor. The maintenance work might be done by a lead operator since there might not be enough maintenance work to justify a full-time position. An office manager might handle some of the accounting work. Quality and engineering functions could be combined.

- Facility – The full cost of the facility might have to be carried at the first level, including rent, utilities to keep it open, insurance, etc.

- IT Costs – If there is an annual license fee for an ERP, this would be assigned at the first level.

Additional levels – The second level might be cell phone chargers, the third level could be screen protectors, and then the fourth segment could be cassette tape cases. Through each one of these segments, all of the resources of the organization need to be assessed and assigned as you build up the business. At Level 2, it might make sense to hire a full-time accounting position and convert the office manager to a purchasing manager.

If, by chance, the order for the second and third segments is switched, you can’t just flip the resources in each of their respective columns. If a maintenance position was added at level 2, but that position also benefits level 3, the maintenance position would still belong in level 2. Please see the summary chart below for the four levels. In reality, I have been involved in multiple situations where there were at least a dozen levels.

It turns out that due to all the additional resources and complexity, plus the low margins, cassette tape cases lose money at that level. The decision is made to discontinue that business and all resources assigned to it are removed. To add a wrinkle to Level 1, you have to consider customers who may purchase products that fall into several categories. Customer A only buys cell phone cases (Level 1), but Customer B buys mostly cassette tape cases (Level 4), and only a few cell phone cases. If you discontinue cassette tape cases, an educated decision is required to determine whether the sales of cell phone cases to Customer B would also be lost. This is an example of how this becomes an iterative process.

There are still many things left unsaid about this process, so next week, we’ll address lessons and pitfalls from zero-base budgeting exercises.